U.S. Faster Payments Barometer: 2023 Survey Results, Part 2

The introduction of FedNow in July 2023 is the latest milestone in the U.S. banking industry’s journey toward faster payments. It’s hard-won progress, as banks have faced considerable challenges when transforming business operations to accommodate a 24/7 model while safeguarding against real-time fraud vulnerabilities.

To better understand the complex factors driving this transformation and the shifting dynamics of payments in the U.S., Volante has sponsored an annual survey of 427 market participants — including financial institutions, facilitators, and network operators — on which this report is based. As the industry propels forward and embraces real-time payments, this report underscores the critical importance of strategic planning and forward-thinking, the challenges inherent to legacy systems, and the need for collaboration with trusted partners.

Last week we shared part 1 of our report; this week, we’re sharing the rest of our findings.

Fraud: A growing concern and a shared responsibility

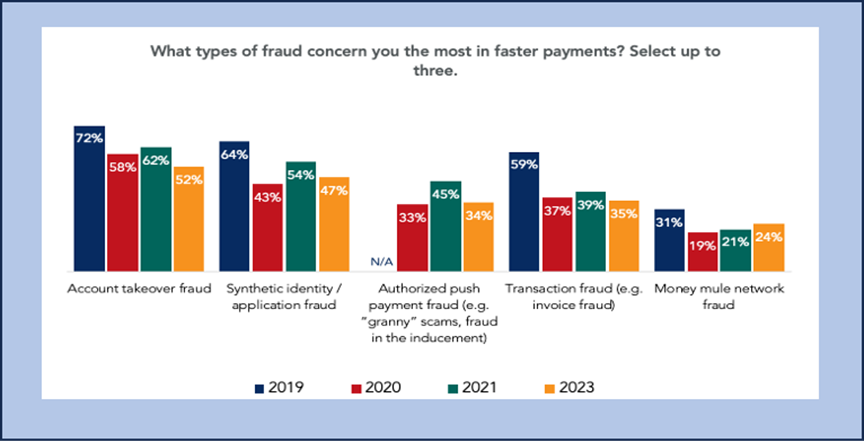

While only 27% of respondents say they’ve seen an increase in fraud related to faster payments, this percentage has more than doubled since 2020. When asked what types of fraud concern them most, 52% of respondents said account takeover fraud, while 47% said synthetic identity/application fraud. Other forms of fraud were mentioned but to a lesser extent.

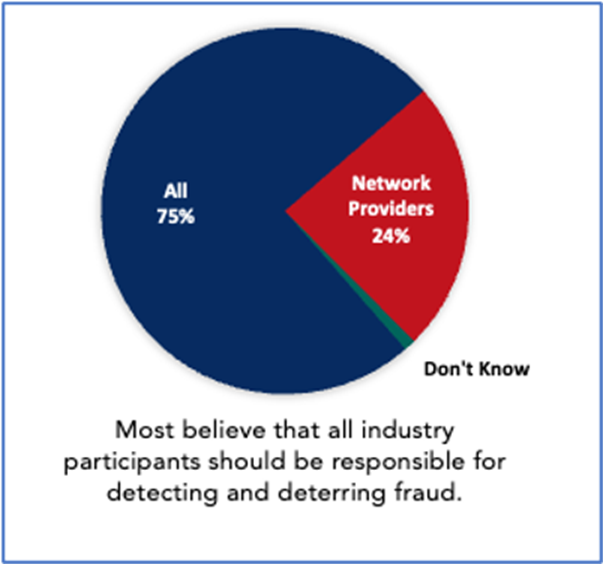

When it comes to detecting and deterring fraud, the vast majority of respondents (75%) agree that all entities across the payments value chain bear responsibility — especially network providers, who almost unanimously (90%) felt this way.

“This is a really interesting point because it highlights that the faster payments ecosystem is at war with fraud,” said Andrew Lang, Managing Partner at Glenbrook Partners — the payments consulting firm behind the Barometer — during a recent FPC Town Hall. “It isn’t specific to one entity in the value chain, but to everyone in the value chain.”

“It’s really important that we promote training and provide educational materials to organizations of all sizes,” Lang added. “Not just the biggest FIs but also credit unions and organizations that don’t have the necessary tools or resources to combat fraud. We’re all in this together, and no one is immune to fraud.”

Demand for digital resolution, cross-border transactions grows

According to 81% of respondents, built-in digital resolution capabilities are a must-have for faster payment systems — a 10-point increase over the past four years of this survey.

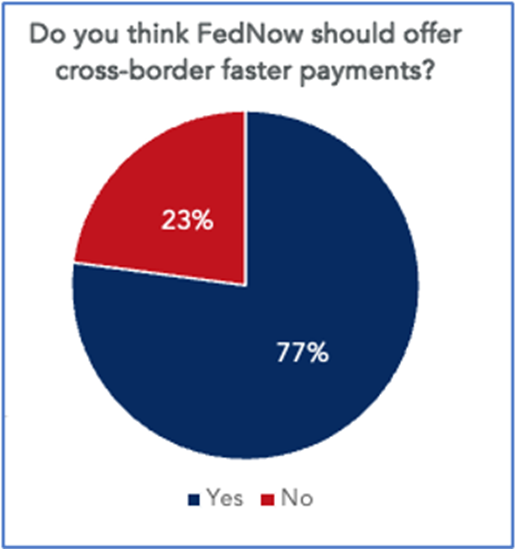

Digital resolution isn’t the only capability that many FIs and businesses deem essential — 39% of respondents say that they are either currently using or plan to use RTP®’s cross-border capabilities. FedNow® users are even more vocal in their demand for cross-border transactions, with 77% of respondents saying that the system should support cross-border faster payments.

77% of respondents think FedNow should offer cross-border faster payments.

“We know that Visa and Mastercard already support faster payments in their credit and push transfers, and we know that the Clearing House with RTP has its pilot which it’s planning to move forward with,” said Elizabeth McQuerry, partner at Glenbrook Partners, during the FPC Town Hall. “From what I understand, FedNow is studying it.”

“The demand is there, but for now the focus is on getting through the first wave of adoptions and implementations within the U.S.,” said Randy Rodriguez, North American regional sales leader for Volante. “As you survey year-over-year, you’re going to see [cross-border faster payments from FedNow] become an increasingly wanted capability, but we don’t see a lot of that right now.”

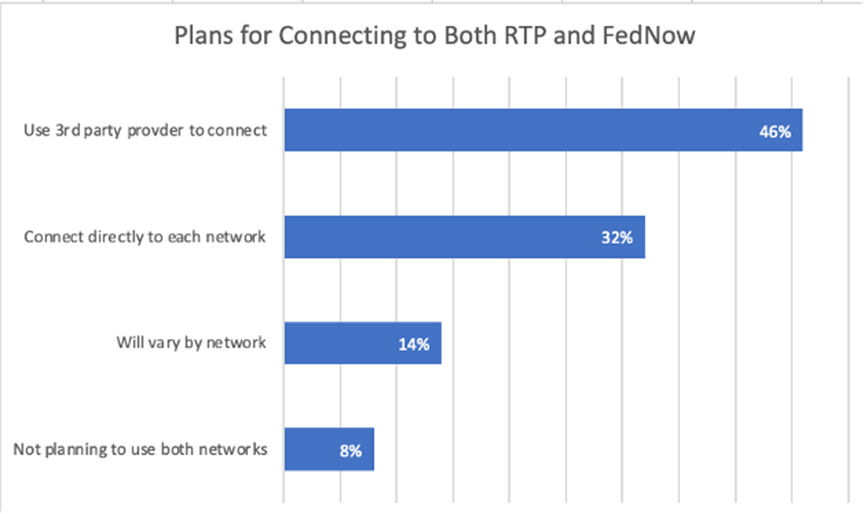

Third-party service providers are the key to faster payments adoption

Integrating and operating faster payment systems such as RTP and FedNow is both complex and resource-intensive. Third-party service providers enable financial institutions (FIs) to overcome these barriers to adoption by:

- Using SaaS-based business models to deliver resilient disaster recovery services and scalability without the need for extensive hardware upgrades

- Managing operations on behalf of FIs, reducing overhead costs, and enabling FIs to focus on innovation and monetization

- Providing the systems and expertise to help FIs adapt their operations to support a 24x7x365 environment and accelerate their speed-to-market

As a result, almost half (46%) of all companies planning to use RTP and FedNow say that they will connect to both systems using a third-party provider, compared to 32% that say they will connect to each system directly.

But faster time to market and lower operating costs aren’t the only reasons a growing number of FIs are turning to third-party providers — many providers also offer value-added services, such as:

- Proxies/aliases for payment initiation

- Payment confirmation notifications for both senders and recipients

- QR code payments

- Online merchant-initiated payments

- Smart routing based on predetermined routing preferences

- Recurring/automatic payments

- Additional remittance data

The results of the 2023 survey show an industry in the midst of transformation, as a growing number of FIs and businesses transition to real-time operating environments for all payment types. With this transition comes new challenges and opportunities — both of which FIs can confidently navigate with the support and expertise of a trusted payments partner.

For a comprehensive view into faster payments adoption in the U.S., access your free copy of the 4th Annual U.S. Faster Payments Barometer here.