The emergence of Payments Modernization 3.0

Alan and Bhaskar were recent guests on our Elevate podcast and are guest contributors to our blog. Alan leads Accenture’s Payment Technology Consulting in North America, while Bhaskar brings nearly 22 years of industry experience with the last decade focused on payment modernization.

Payment systems are in the middle of a transition that touches all aspects of a bank’s payment operations. This article explores what we call “Payment 3.0” and offers practical guidance for organizations navigating this shift – a transformation that’s already well underway.

From the stone age to the digital age: understanding payments evolution

The payment industry’s journey over the past two decades tells a story of continuous evolution. What began as “Payment 1.0” with specialized engines for traditional payment types has transformed through “Payment 2.0” with service-oriented architecture to today’s “Payment 3.0” – characterized by cloud-native, API-driven microservices designed for real-time processing.

Three consistent forces have driven this change: financial institutions updating legacy systems, payment providers evolving their platforms, and regulatory bodies imposing new requirements. ISO 20022 represents what we consider a watershed moment, forcing institutions to reconsider their entire approach to payment processing.

What’s driving Payment 3.0?

In our consulting work, we’ve identified two primary drivers creating the need for Payment 3.0. First, we’re seeing bank clients’ business models fundamentally changing. Corporates that once primarily dealt with suppliers and vendors are increasingly shifting to direct-to-consumer approaches. This evolution demands support for credit card payments, digital wallets, real-time payments, and P2P solutions like Zelle.

The second major driver is the increasing demand for data intelligence and AI. Payment data has been heavily underinvested in for too long, with many financial institutions only now recognizing its potential for delivering insights and enhancing customer experiences.

The integration challenge

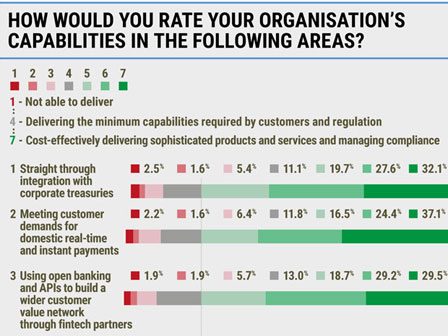

One consistent hurdle for financial institutions is managing integration with legacy technology. In fact, in a recent payment modernization survey conducted by our firm, banks identified the accumulation of integration services as one of their top technical gaps.

For larger institutions, these overlapping services create significant operational costs that become increasingly difficult to justify. The root cause often stems from a lack of holistic integration planning, with each solution added independently without considering the broader landscape.

Why real-time changes everything

Real-time payments have fundamentally challenged traditional payment architectures. While Payment 1.0 and 2.0 systems were built for processes like ACH and wires – with complex business rules and acceptable processing times in a T+1 or T+2 world – real-time payments demand near-instantaneous response.

This shift creates what we view as a perfect storm for technology. Where legacy infrastructure might handle 100 transactions per second, real-time systems often need to process thousands in the same timeframe. The combination of faster processing, potentially higher volumes, and new direct-to-consumer business models requires not just new payment engines but a complete ecosystem rethink – including sanctions screening and fraud detection systems that can keep pace.

The data dimension

Based on our experience with ISO 20022 migrations across multiple institutions, we believe this shift is about far more than message formats. It affects interactions between financial institutions, corporations, and clients, requiring banks to examine their complete payment infrastructure.

Consider payment reconciliation: organizations receive millions of payments daily, often with cumbersome invoice reconciliation processes. ISO 20022’s structured format can mandate specific information like invoice numbers, making downstream processing significantly more efficient. However, realizing these benefits requires customer involvement from the start, as they must adapt to leverage the new capabilities.

Keys to successful Payment 3.0 modernization

Based on Accenture’s experience with numerous financial institutions, successful payment modernization requires more than just technology selection. Consider these essential approaches:

- Strategic sourcing decisions: We advise our clients to “buy the commodity, build the differentiator.” Use payment platform providers for core processing while maintaining control over your business rules and customization.

- Service customization: Rather than customizing platforms, we recommend focusing customization on services. This approach allows quicker adaptation to changing client needs.

- Ecosystem thinking: Consider how related systems – from fraud detection to sanctions screening – must evolve alongside your payment capabilities.

- Customer involvement: Engage customers early in your modernization journey, particularly for ISO 20022 initiatives, helping them understand how to leverage enhanced data capabilities.

The time for action is now

The urgency of embracing Payment 3.0 cannot be overstated. By Accenture’s calculations, the industry has already been in the Payment 3.0 era for a year or two. What begins as a competitive opportunity quickly becomes a necessity for survival.

When starting your modernization journey, we recommend these practical steps: assess your current technical debt, map out regulatory requirements, identify differentiation opportunities, develop a clear roadmap with business outcomes at the center, and invest in teams with both technical and business payment expertise.

In our experience, successful payment modernization isn’t about technology for technology’s sake – it’s about enabling your institution to serve customers better, adapt to market changes, and maintain competitive advantage in an increasingly complex ecosystem. The organizations that thrive will embrace this new reality with strategic vision and decisive action.

Listen to our full conversation on the Elevate podcast for more insights on the evolution of payments infrastructure.